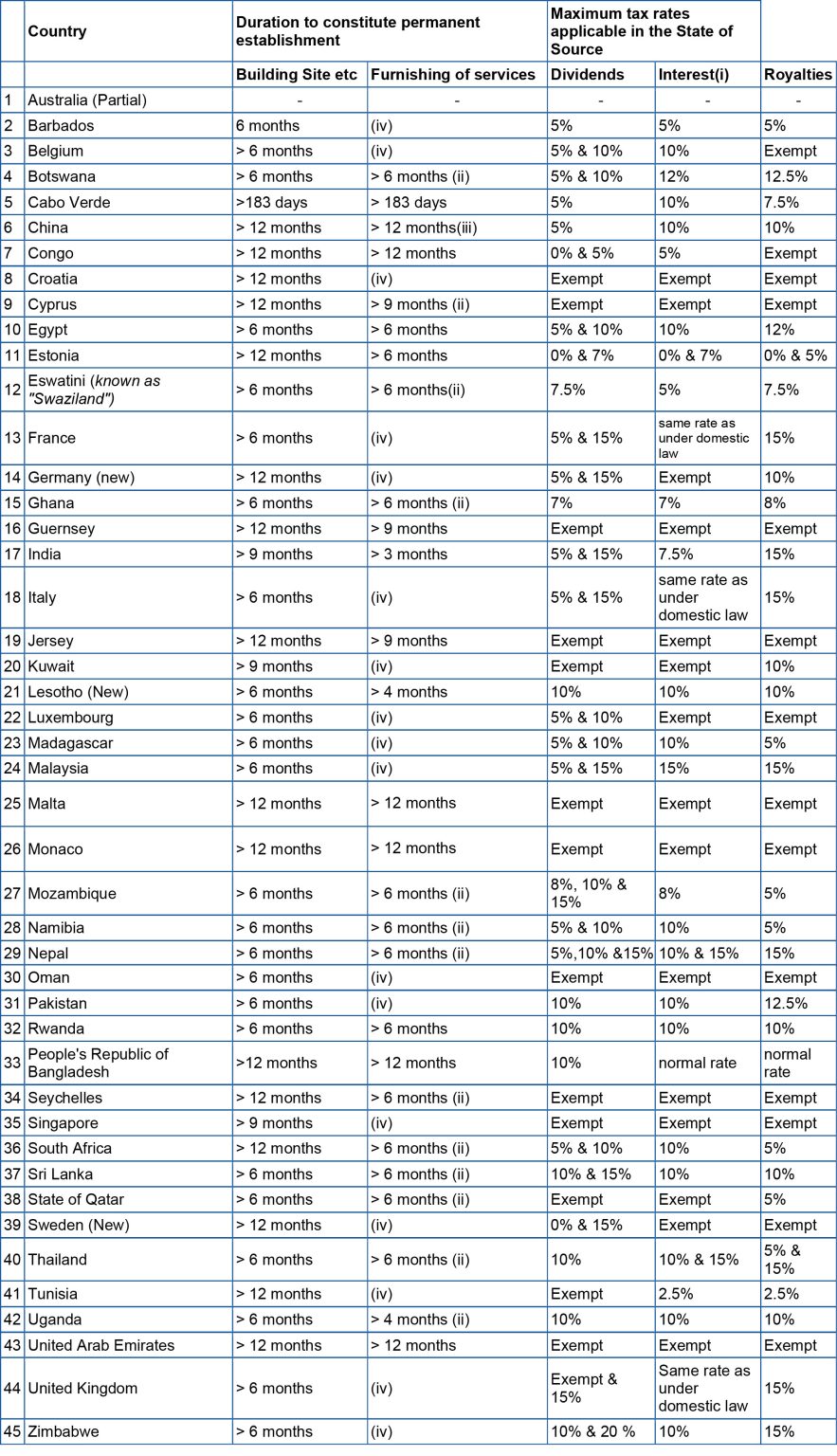

where interest is taxable at rate provided in the domestic law of the State of source or at reduced treaty rate, provision is usually made in the treaty to exempt interest receivable by a Contracting State itself, its local authorities, its Central Bank/all banks carrying on bona fide banking business and any other financial institutions as may be agreed upon by both Contracting States.

within any 12-month period

within any 24-month period

no specific provision made in respect of furnishing of service